Mortgage Rates Today: Unpacking the Trends & Seizing Your Opportunity

Dr. Aris Thorne's Article:

The 6% Mortgage Rate: A Portal, Not a Prison

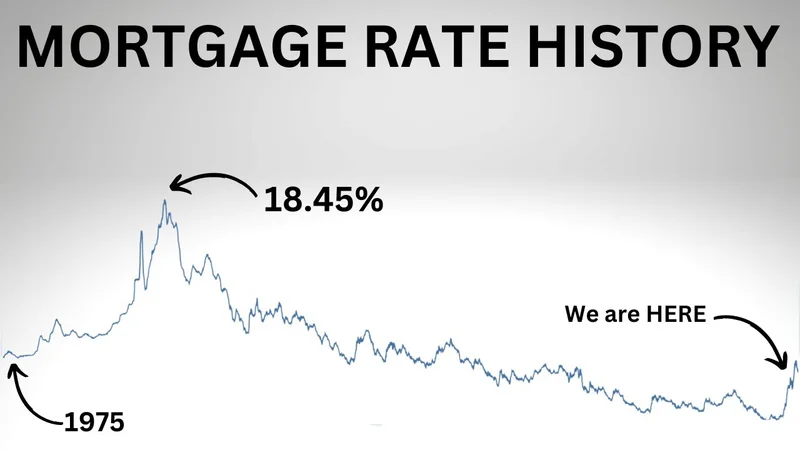

Okay, friends, let's talk mortgage rates. I know, I know – the words alone can induce a financial coma. But before you glaze over, hear me out. We're seeing 30-year fixed rates hovering around 6%, and while that might not sound like a party compared to the rock-bottom rates of a few years ago, it's not the end of the world. In fact, I see it as a fascinating inflection point. A chance to rethink our approach to homeownership and wealth building.

Think about it: for generations, the "American Dream" has been inextricably linked to owning a home. But what happens when the traditional path feels… less accessible? Less like a dream, more like a daunting climb? That's when we innovate. That's when we get creative.

We've been so focused on the rate itself, we haven't stopped to consider the bigger picture. A 6% rate isn’t a wall; it's a doorway. It’s a prompt to ask ourselves, "How can we make this work smarter?" Are there ways to leverage shorter-term loans, like a 15-year fixed, to build equity faster, even if the monthly payments sting a bit more upfront? (Yes, absolutely – you’ll save a fortune in interest, and you’ll own your home outright much sooner.) Or what about exploring adjustable-rate mortgages (ARMs) if you know you won't be in the property long-term? It’s not for everyone, I get it, but knowledge is power.

And let's not forget the power of good old-fashioned financial literacy. I saw a comment on a Reddit thread the other day that really resonated with me: "People complain about rates, but are they even budgeting properly? Are they maxing out their 401ks? Are they negotiating for better salaries?" It’s harsh, maybe, but it’s a valid point. Mortgage rates are just one piece of the puzzle.

The Fed's actions are also playing a crucial role. They've been carefully calibrating interest rates, and while economists don't foresee massive drops before the end of the year, the expectation is that rates will ease a bit lower in 2026. The Fed is considering another rate cut before the end of the year. The CME FedWatch tool predicts a roughly 85% chance of another quarter-point cut at the next Fed meeting in December. Current Mortgage Rates: November 25, 2025.

Here's where my MIT brain kicks in. I see parallels between this situation and the early days of personal computing. Remember when computers were these massive, expensive machines accessible only to big corporations and universities? Then came the personal computer revolution. It wasn't about making the existing computers cheaper; it was about making them different, more accessible, and more user-friendly. We need a similar shift in thinking about homeownership.

What if we started prioritizing community-led housing initiatives? What if we embraced innovative financing models that bypassed traditional banks altogether? What if we focused on building smaller, more sustainable homes that required less upfront capital? These aren't just pipe dreams; they're real possibilities that are already gaining traction.

And the technology is there to support it. Imagine using AI-powered tools to optimize your mortgage strategy, predicting rate fluctuations and identifying the best possible loan options tailored to your individual circumstances. Or leveraging blockchain technology to create decentralized, peer-to-peer lending platforms that cut out the middleman and offer more competitive rates. The possibilities are truly endless.

Of course, with all this innovation comes responsibility. We need to ensure that these new approaches are equitable and sustainable, that they don't exacerbate existing inequalities or create new risks. But I firmly believe that the potential rewards far outweigh the risks.

When I look at the current mortgage landscape, I don't see a crisis. I see an opportunity. A chance to redefine the American Dream for the 21st century. A chance to create a more inclusive, more sustainable, and more innovative housing market that benefits everyone.

The Future Isn't Just Affordable, It's Ingenious

Let's be frank: complaining about rates gets us nowhere. It’s time to embrace the challenge, to unleash our collective ingenuity, and to build a future where homeownership is not a privilege, but a portal to opportunity for all.

Related Articles

Cloudflare (NET) Stock Analysis: What's Driving the Surge and Is the New Price Target Justified?

The Contradiction at the Heart of Cloudflare's Rally There are moments in the market when a company’...

PLTR Stock: Cathie Wood Sells, But What's the Big Picture?

Dr. Thorne: Forget the Doubters—Palantir's AI Surge is Just the Beginning! Okay, friends, buckle up....

Comcast's Stock Is Finally Paying the Price: Why It's Tanking and the Corporate Excuses You're Supposed to Believe

A Confession, Not a Notice So, Comcast’s stock took a little dip the other day. Wall Street gets the...

Arm Stock: Bullish Forecast? Yeah, Right.

Generated Title: Arm's AI Forecast: Or Just More Silicon Valley Hype? Okay, Arm's giving us the ol'...

Bitcoin: Fed's $29.4B Injection – What the Hell Does It Mean?

Okay, so the Fed injected almost 30 billion bucks into the banking system last Friday. $29.4 billion...

Crypto Market Faces Headwinds: Analyzing the Macro Signals Driving the Dip

Generated Title: Bitcoin's Silent Standoff: Why a Sideways Market Masks a Brewing Storm The chatter...